Get an instant access to up-to-date metrics at low cost

Bank's current systems and issues

Today, Retail and Private Banks' Core Banking System (CBS) and Portfolio Management System (PMS) are strong assets. They have matured over the years and are often a very solid basis for the rest of the satellite IT systems. They are used to efficiently manage the basic core banking data, like clients, portfolios, their security composition, the pending orders, the market transactions and so on. Portfolio-level and bank-level consolidated metrics however are often based on long running algorithms and are therefore executed either during end of day batches or on-demand, meaning users' have to work with more or less outdated data or data that is long to get.

The issue is that in recent years, banking has seen several shifts:

- An ever faster market (more actors, algorithmic trading, easier access to information)

- A growing pressure on returns. Clients want reliability, while banks need to lower their margins due to competition

- A complexification of the products to try and manage risks while meeting clients growing sophistication

- The increasing regulatory pressure impacting margins, efficiency and attractiveness

All of this has underlined an increasing need for up-to-date consolidated information (exposures, performance, variance, volatility, ...) at different levels (position, portfolio, desk, region, bank). While some of this complexity has already been addressed in Investment Banks (IB), Retail and Private Banking have lagged behind, mostly because the need was initially not identified as so important but more importantly because they lack the resources. Indeed the IB solutions are generally plagued by a very high TCO (Total Cost of Ownership) that is neither justified nor bearable for other kinds of banks.

An example - Portfolio variance

One of the core metric used by portfolio risk managers is the portfolio variance. To calculate a portfolio variance over a time period, one needs to compute the variance of each of the securities held on the time period, their correlation with one another (covariance) and to aggregate them based on the security relative weights in the portfolio. Because this metric needs to integrate a lot of heterogeneous values (numerous security prices, portfolio compositions, forex rates) it generally takes seconds, if not minutes, to compute on classical systems (in some big institutional portfolio scenarii, it even happens that the CBS or PMS cannot do the computation). This is because

- A lot of data needs to be retrieved

- The dataserver, generally a unique central database, is usually suffering from a lot of contention since it supports the whole operational work of all the banks' users

- And the computation itself requires a lot of operations, which puts strain on the application server (again, oftentimes, there is only 1 or 2 of those for the entire user population)

Thus, running such heavy computations on the online system adds an unmanageable additional level of contention, lags, slownesses for the users (and sometimes directly for the clients who access data through the e-banking portal for example). And those are the main reasons why banks are struggling with portfolio risk management: the system is not helping the risk managers enough by providing them with the right information at the right time.

Most of the attempts to solve for this problem in the operational system have failed because it either

- Tries to keep the database as a central component in the architecture, and it creates an unmanageable amount of contention and transactions (too much volume to process)

- Or it tries to load every single relevant thing in memory (several GB) at startup on a single node meaning that the server takes hours to start, and is a single point of failure

Another often seen approach is to go through Business Intelligence (BI) components. It is however not perfect either, as it is mostly based on overnight computations on frozen data, which does not fit our stated need for up-to-date, near real-time metrics.

Most of those issues or limitations come from choices that were made based on the available technology and the available budget at the time. But today, a lot of those parameters have changed. Led by the needs of the internet giants and the increased capacity of commodity hardware, new kinds of technologies and architectures have emerged and it is now possible to build within the operational system very efficient ways to perform heavy computations on massive amount of data.

A New Hope

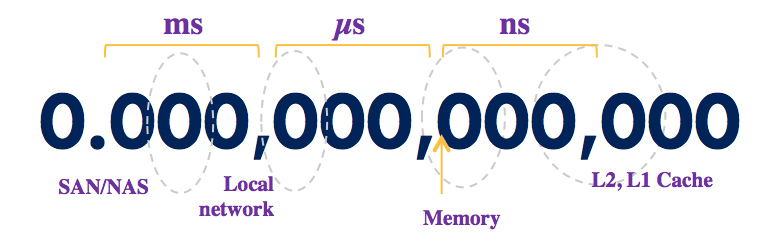

Data access has a cost, and as is well known, typical disk solutions (SAN or NAS) are the weakest link when it comes to throughput speed, and nothing beats local RAM.

Hardware throughput time

The first thing is therefore to realize that the increased capacity of commodity hardware at a low premium gives access to a lot of RAM as well as accompanying local computing power for a very low cost of ownership.

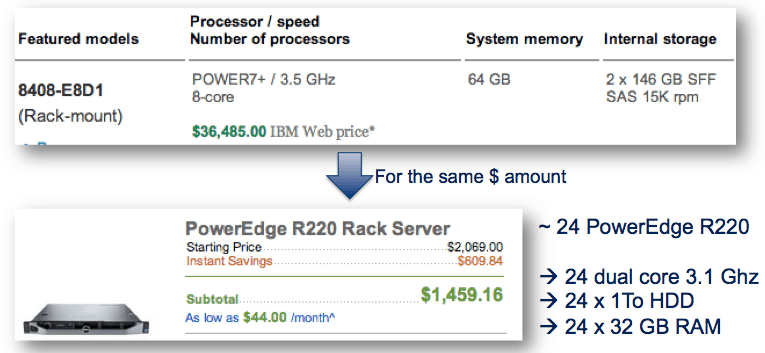

AIX vs Dell Cost

This comparison is a shortcut that we can't really make because you don't get the same support or quality between the 2 products, but it gives a good appreciation of the cost difference between typical servers and commodity hardware

Distributing data and computation is a direct consequence of this trend. While massively distributed processing was reserved to giants (Research institutes, major internet companies), cheap hardware now makes it available to everyone. This allows any IT department of any size to consider grid computing solutions nowadays. And in turns, this ended up with the creation of numerous distribution frameworks that give those setups a level of reliability that is expected from classical server/mainframe.

Commodity hardware and new distribution frameworks therefore make grid storage and grid computing the key basis for a fast, highly available, highly reliable and cheap system.

While those new concepts were key to solve the problem at hand, in our particular case, a paradigm shift in the system architecture was also necessary to achieve the best result possible. The classical paradigm is a pull model (intraday values are computed on-demand) but we are now going to look at some kind of push based one. Indeed, while with a pull model one can consider adding resources to try and bear the load, it is still very difficult to give users fluid and reactive interfaces but more importantly, it is not possible to build proactive systems that will react on thresholds because the consolidated data is just not there! This is actually not a new paradigm but it is definitely novel in the banking industry.

A proposed solution for our use case

Thinking about what would be an ideal world for our risk manager. We can see 2 main axis:

- Data visualization. The risk manager first wants to have access to an up to date dashboard containing all the KPIs he needs, as, for instance, the simplified example of the portfolio variance presented here. He also wants this to be a fast dashboard, not a background report that runs for a few minutes. But he also wants to be able to play with it and have instant return. Scenarii include changing the time window used or removing an outlier value from the KPI calculation. Here is an example of the kind of dataviz done nowadays and that users more and more expect from their systems at work.

- Alerting. Coming up with a system that provides always up-to-date KPIs, it is possible for risk managers to define alerts based on thresholds, or more complex criteria. They will then be able to react quickly to impacting market events.

Think about volatility for example. A portfolio manager might want alerting level on volatility. In the case of long term trading, he might want to move away from a security that becomes volatile. In the case of tactical trading, he might rather wait for a high volatility time to try and trade during the peaks.

Once a distributed architecture is chosen, the challenge is to make it highly available. Indeed, commodity hardware will fail, and software solutions are therefore used to cope with that. Partionning and replication are the keys here and will be provided by a software solution (in our case we chose Infinispan) that will be configured (typically the replication factor) depending on performance consideration and most importantly on the cluster topology.

The second thing is about changing how systems are built in banks. Rather than staying with a single type of paradigm, best of breed architectures must be considered for each use case. Banks classically only build systems based on a pull model. They have a strong data layer, and when some consolidated data is needed, the computation is done on the fly. To improve response time, some consolidations are made and persisted in batches (often overnight) but that means the user accesses outdated information (think back on the volatility use case from before). The shift is therefore to open the information system to other architectures, and in the considered use case, to introduce a push one where consolidated values are constantly recalculated and the user just gets instant access to the latest computed data, that is generally only a few seconds old at most.

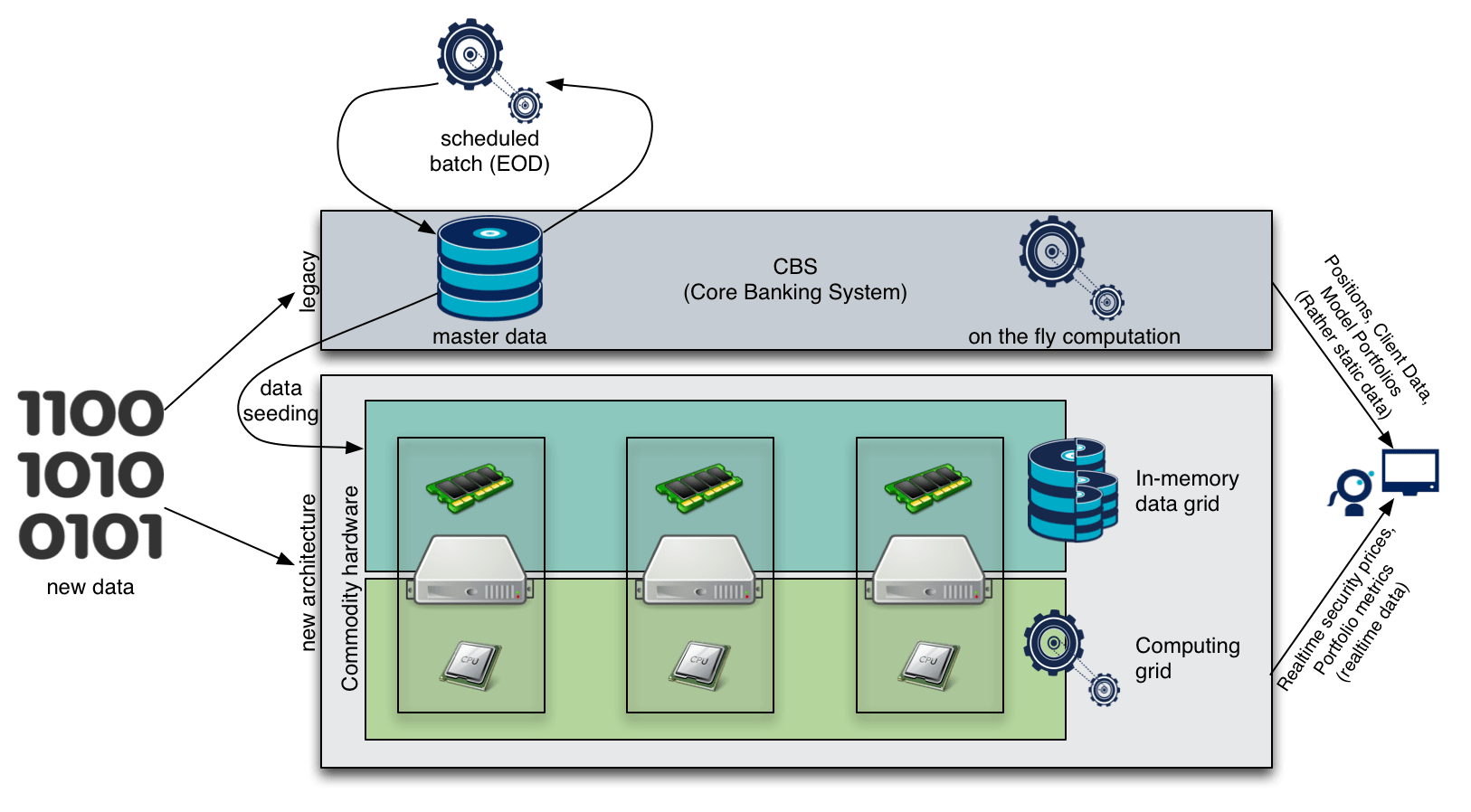

Proposed Architecture

This type of infrastructure combined with the following software architecture design will have several benefits:

- Fast access to data. Data being in memory (RAM), the latency to access it is extremely low. This allows for quick computation cycles when metrics are constantly recalculated, but it also provides fast response time for request on data that might still need to be computed on demand (it is not possible to precompute and keep up-to-date every single metric and every single scenario)

- Parallel processing. The grid setup enables the use of numerous CPU that can work in parallel. Moreover, the computing nodes and the data nodes are the same which means that the computation can happen on local data, without incurring any penalty due to data communication over a network (which as shown is an order of magnitude slower than local memory). Portfolio variance for example, which is based on individual instrument variance and covariance, is a good candidate for such a setup.

- Reactive architecture. Those KPIs are dependent upon market events. For example the portfolio variance will depend on security price, that impacts the security variance and covariance, and transactions, that impact security weights in the portfolio. Those market changes will trigger a recalculation of the metrics for the impacted portfolio (rather than simply recomputing everything on a schedule).

- Incremental calculations. To compute many of those metrics, a lot of operations are required. Portfolio variance will require to compute the variance of each security, then the covariance of each security with all the others composing the portfolio and so on. This is computationally intensive and would be costly if done on every impacting market change. However, a lot of those metrics can be calculated, or sometimes approximated incrementally. This means that from a KPI and a market indicator change (e.g. a security price), the new KPI value can easily be computed (a few operations only) from its old value and the parameter change.

Each of the benefit of our architecture as presented above is key in addressing the needs of our use case, and their combination is what makes the end system achieve the desired efficiency.

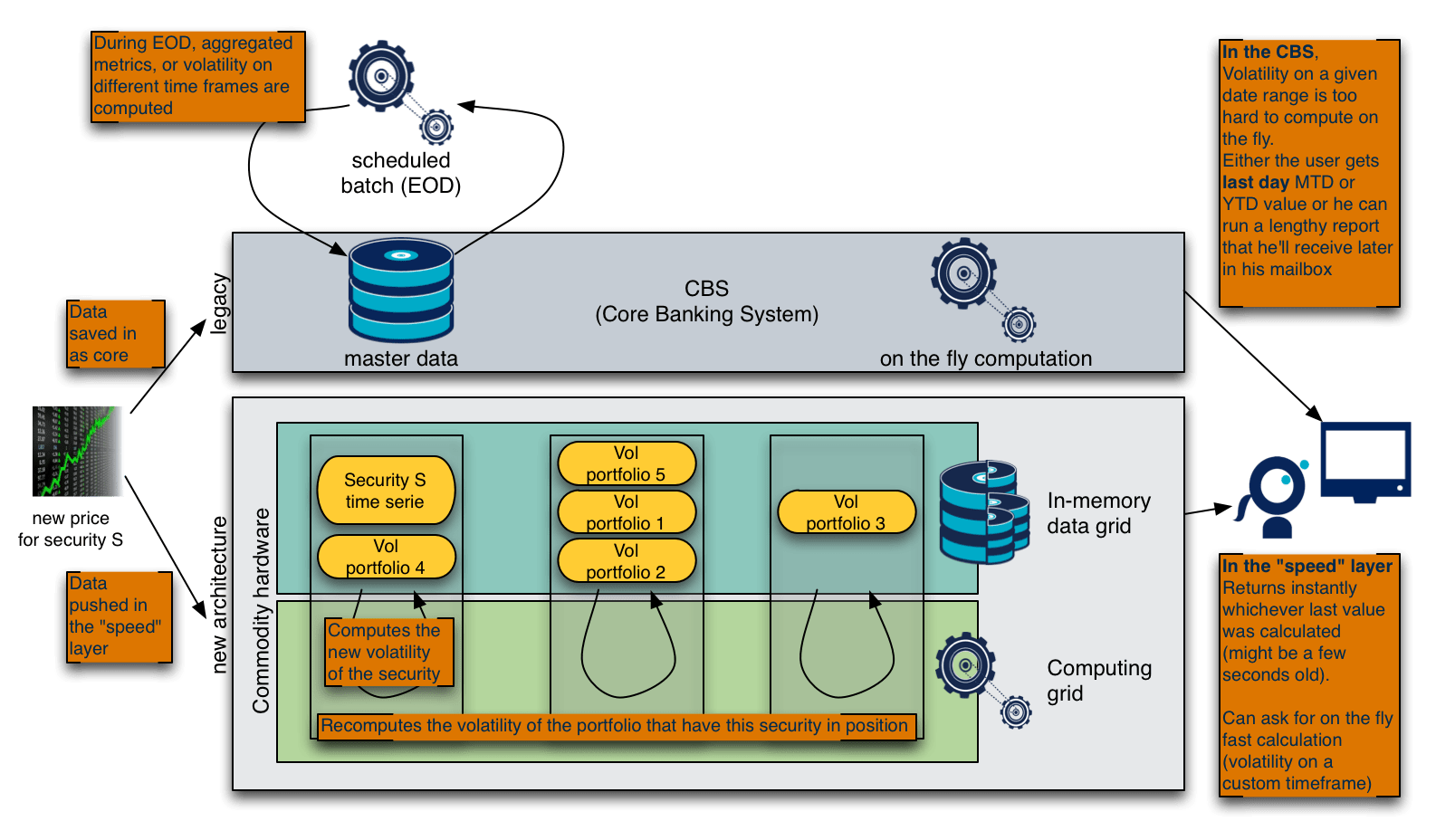

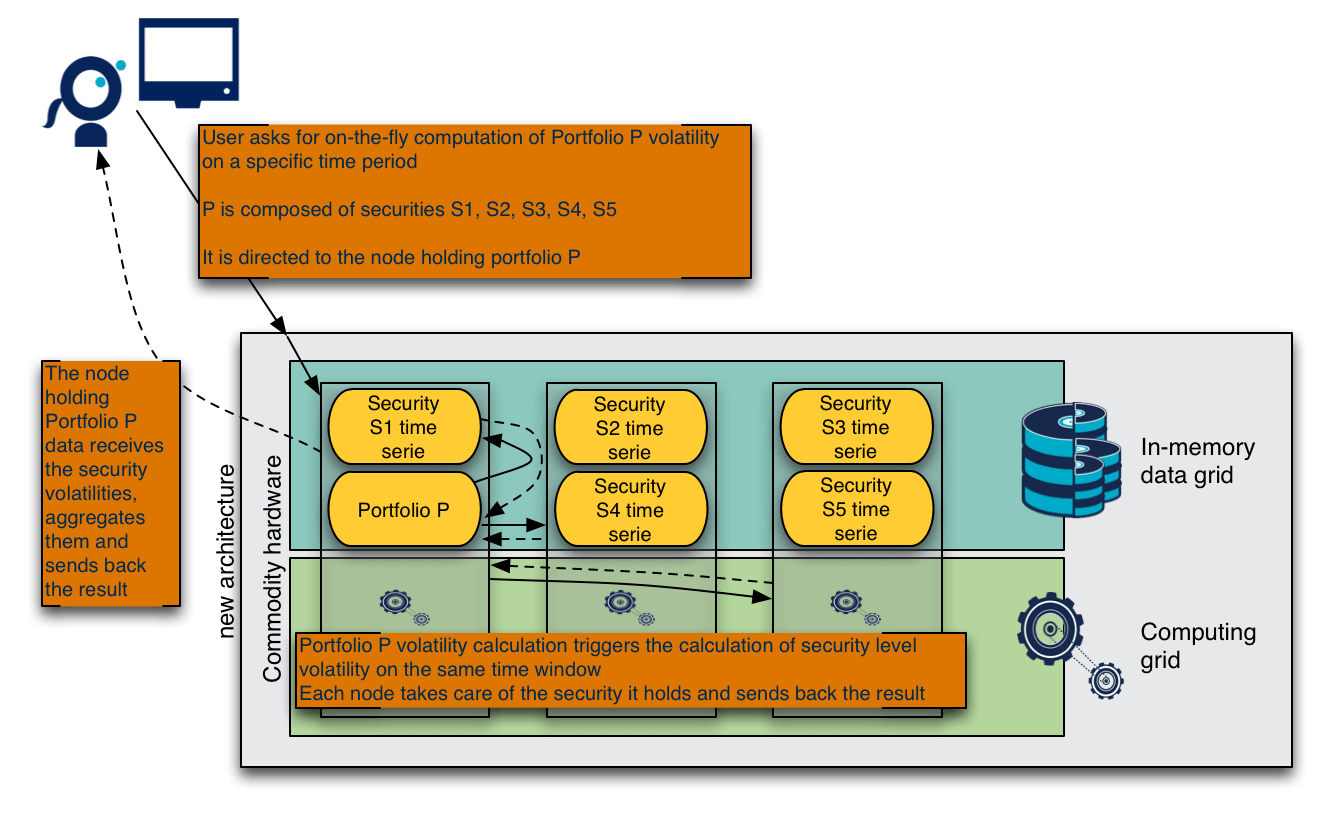

Here is what such an architecture would look like in the described volatility use case

Reference data processing

Near-real-time processing of live data

A prototype and the learnings we extracted

With these considerations of data grid, computing grid and reactive architecture in mind, we chose to try the Infinispan product (aka JBoss Data Grid). It was a trending product and had been chosen by JBoss as their main data caching product. Additionally, some of the latest grid computing features looked promising and we wanted to test it in a real life use case. We therefore implemented a prototype containing: a data-structure, a "market simulator" to fake a reuters pricing feed, and we implemented the calculation of the portfolio performance and the security variance (describing this prototype is not our point here and will be the subject of a future article). Those were interesting proof of concept since while still easy enough to implement, they required a fair amount of computation and could be easily scaled to a large number of portfolios to test our setup.

We have learned several thing:

- Low cost architecture. This is indeed a low cost solution. We used a JBoss application server (free) with the Infinispan cache technology (free). Our example ran on a developer machine emulating a cluster of 2 servers, with great performance. There is no reason to deploy the application on highly resilient machines as Infinispan manages the replication and high availability, making the system fault tolerant.

- Structure the data. Organizing data on a grid means structuring it very differently to take full advantage of the distributed storage and computing. The fact that the data is serialized a lot between nodes also drives some of the choices. The goal is generally to not stream data, but only results between the nodes. The main teaching is that data organization needs to be balanced in size and in number between the nodes. In size, because with nodes of generally the same size, they should be filled equally; and in number because when distributing a computation, each node should have about the same amount of work to perform. Additionally, like any key/value NoSQL store, Infinispan imposes limits (object hierarchy, data lookup) that requires to be balanced by careful data modelization.

- Manage the concurrency. Obviously such systems receive a very high volume of events (Reuters can generate upwards of 100'000 notifications per second) and we have discussed that this was the main issue with a centralized database model that can't cope with the transaction volume generated. This equally means that transactions cannot be used in the cache technology. To preserve the consistency of the data, we must therefore use new techniques. One (over-) simplified solution we could work with in the context of our prototype was the notion of "single updater". The principle is simply to say that while each event triggers a new thread that stores the change and can realize some data crunching, only a single thread is responsible for collating all those events and intermediary results and then updating the KPI values. It is worth mentioning that in a "real life" implementation, this single threaded update model would need to be given a lot of thoughts to maintain its virtues, typically to prevent it from becoming a bottleneck (for example having an updater thread per data type). Another approach would be to look into the new reactive frameworks (e.g. Akka).

- Know the product. Infinispan is a complex enough technology that is made to answer several possible use cases. That means that it has a lot of possible configurations and that the defaults are likely not best for a given situation. You need to learn the product to not fall into traps. For example, the constant serialization in the grid setup has made us use an immutable pattern on our business objects to ease development.

If you have more questions about this, be sure to leave a comment, and continue following our blog, there should be a technical article on Infinispan coming in a few weeks.

To sum up

New paradigms that have emerged in the recent years have allowed for a new class of applications/frameworks. Those have for the main part not found their way yet in the Retail and Private Banking sector but they should. We have seen that by using commodity hardware, those solutions are cheap. Through new architecture, they are made resilient and extremely performant. Finally, they are easy to put in place as they are not intrusive. The solution mentioned above is simply reading from the core banking data, never writing. And it exposes data in services that any front end (like an existing PMS) can consume and overlay on top of the core data coming from the Core Banking System (CBS). This simplicity makes this kind of system easy to setup in existing environments, alongside the CBS, that is by the way not meant to be replaced as it holds the master data and is the ultimately trusted source (especially if some of the realtime metrics are only approximated).

I'll conclude by opening a new door. Nowadays, additional focus is put on risk management and in particular on credit management. An architecture as described above can be fully leveraged to realize what-if scenarii, simply by faking the inputs (market events) in the system. While banks are today building complex what-if systems completely separate from their core banking one, the kind of platform we described before enables a smooth integration of the online platform and the what-if simulation, which of course means a lot less development and maintenance work.